Weekly Market Update: 11 February 2026

Capitulation Signals Emerge as Bitcoin Tests Cycle Structure

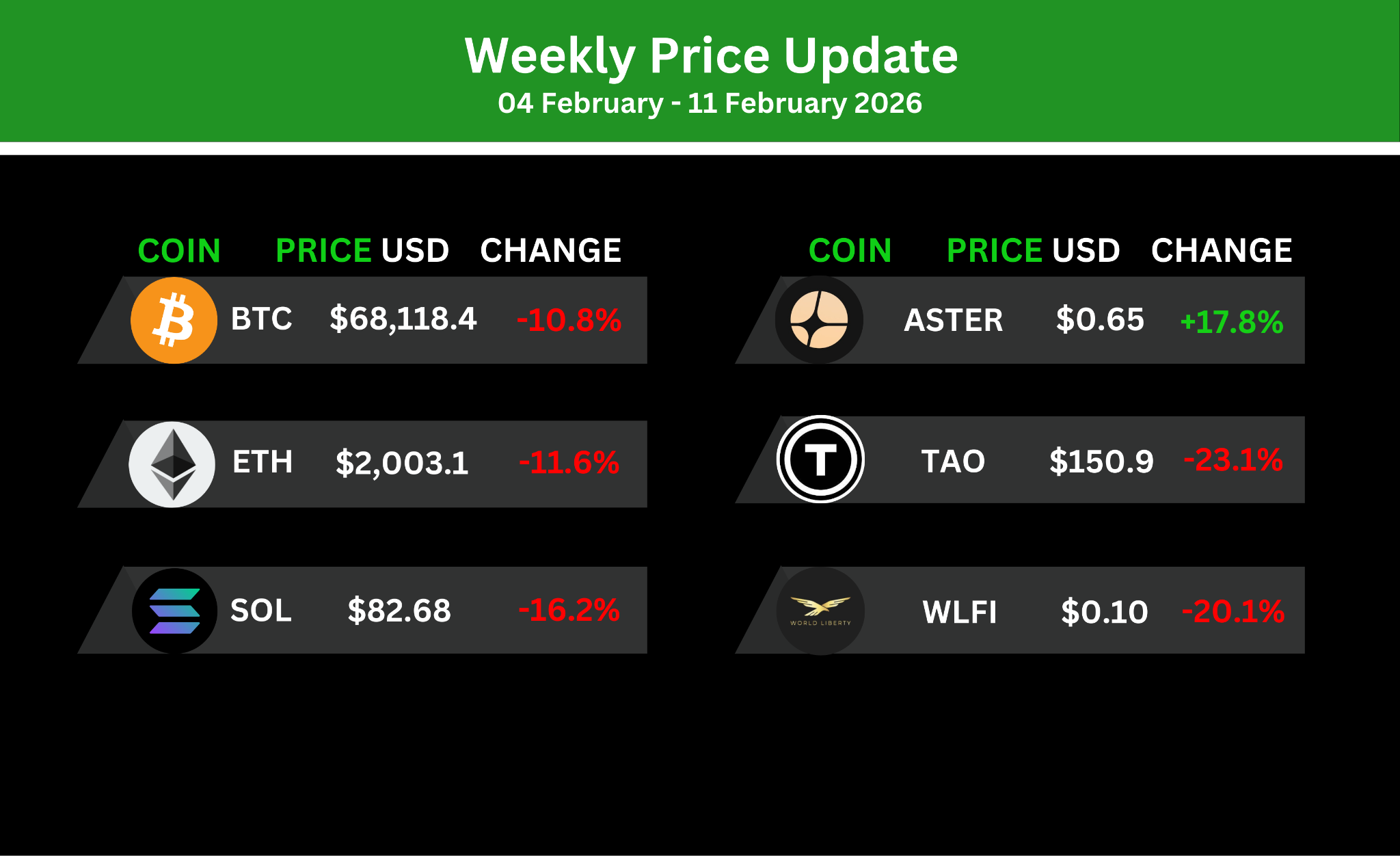

Crypto has continued to slide deeper into bear market territory this week, with Bitcoin breaking into the $60K region and falling back below the previous cycle’s all-time high. The move marked one of the sharpest sell-offs of this cycle, dragging the broader market lower alongside it. Bitcoin closed down ~9% on the week, Ethereum slipped below $2K losing ~10%, and XRP fell ~11%, reinforcing the breadth of the drawdown across majors.

Sentiment has deteriorated quickly, with fear readings returning to levels typically associated with late-stage bear phases. Structurally and psychologically, the cycle is beginning to resemble more traditional patterns rather than the “structural decoupling” narrative seen earlier in the year. Below, we break down the on-chain positioning, spot absorption data, and structural signals that matter most from here.

CLARITY Act Talks Stall, Pressure Ramps Up

Negotiations around the CLARITY Act intensified this week after a second closed-door White House meeting ended without an agreement. While no deal was reached, talks have not broken down. In fact, continued engagement suggests the debate has narrowed to a single unresolved issue. With Senate momentum at risk and legislative calendars tightening, the White House is now pushing for compromise language before the end of February.

The core sticking point remains stablecoin yield. Major U.S. banks, including JPMorgan, continue to argue that yield-bearing stablecoins threaten traditional deposits by functioning as a parallel banking system. Banking groups warn that trillions in deposits could be at risk if yield remains permitted. Crypto firms see the issue very differently. Stablecoins have become core infrastructure, not a side product, with platforms like Coinbase now generating over $1B annualised revenue tied to stablecoin activity. That divergence has put yield at the centre of the standoff.

The GENIUS Act already prohibits stablecoin issuers from paying interest directly. What remains contested is whether exchanges and platforms can continue distributing rewards funded by reserve income, the loophole banks want closed. Treasury Secretary Scott Bessent publicly accused some crypto firms of blocking progress, escalating the dispute and making yield the clear final blocker. If negotiations were going nowhere, repeated meetings wouldn’t be happening. Continued talks signal pressure is rising on both sides to resolve the issue.

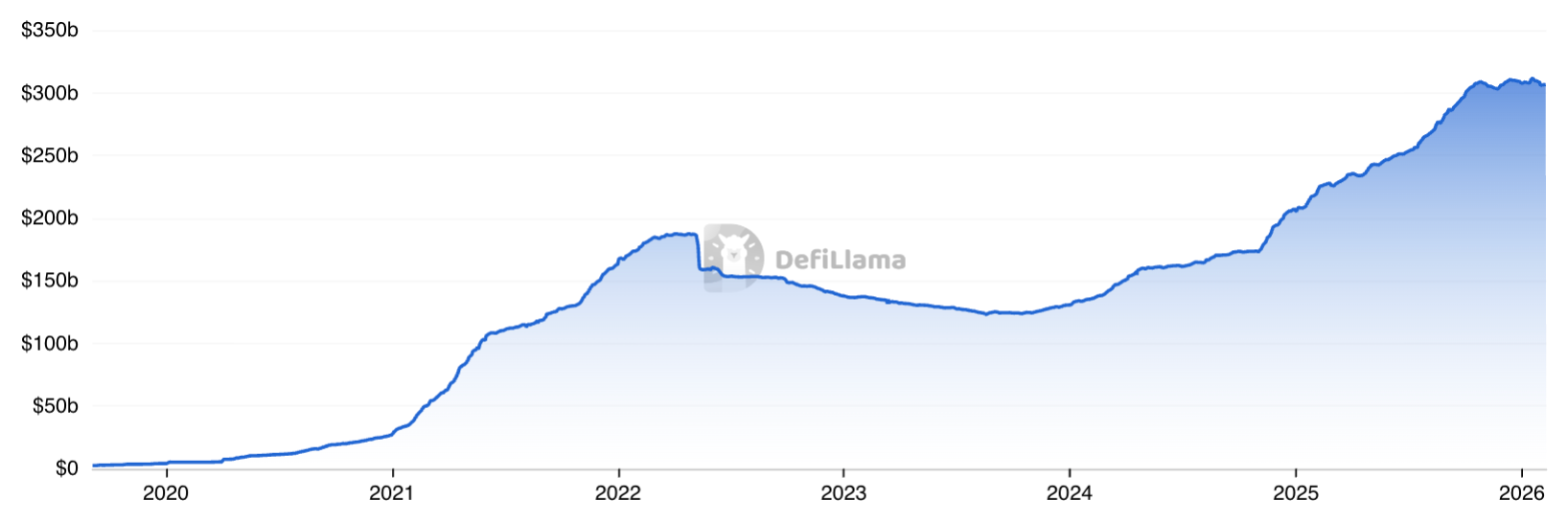

Total Stable Coin Market Capitalisation 2020-2026

- Stablecoins have grown from ~$5B in 2020 to over ~$305B today, a 60x expansion in just over 6 years. This explosive growth is why stablecoin yield has become the single biggest blocker in U.S. crypto regulation, with banks increasingly threatened by the risk of capital moving out of low-yield deposits into higher-yield crypto rails.

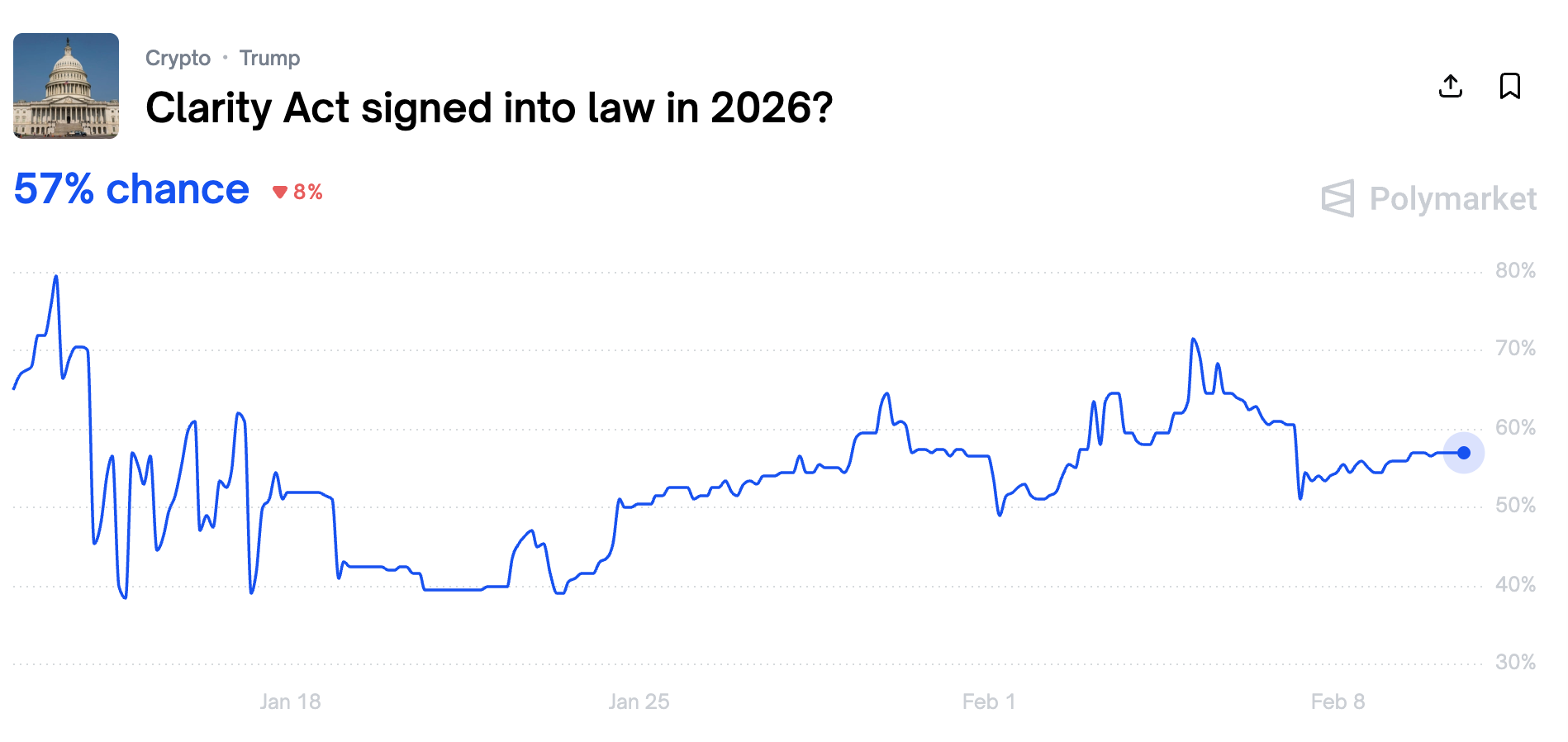

Why this matters is straightforward. The House passed CLARITY in July 2025, and without agreement on yield, the bill cannot advance through Senate markup or reach the floor. Prediction markets currently price roughly a 57% chance of CLARITY becoming law in 2026, reflecting uncertainty. A resolution would finally give the U.S. a clear crypto rulebook, unlocking institutional participation, reducing enforcement-led risk, and accelerating crypto’s transition from speculative markets into core financial infrastructure.

Goldman Sachs Expands Crypto Exposure in Q4

Goldman Sachs increased its crypto exposure in Q4 2025, according to its latest 13F filing released in early February. The firm disclosed approximately $2.36B in total digital asset exposure, broken down as $1.1B in Bitcoin, $1.0B in Ethereum, $153M in XRP and $108M in Solana.

This allocation now represents roughly 0.33% of Goldman’s ~$811B in reported 13F holdings, marking a ~15% quarter-over-quarter increase, despite broader market volatility.

While 0.33% may sound small, the absolute capital involved is significant. If Goldman were to increase its allocation to just 1% of reported holdings, that would equate to roughly $8.1B in crypto exposure. Even incremental moves toward that level would represent multi-billion dollar inflows into the asset class.

Crypto remains one of the few asset classes where retail participation preceded institutional scale. The key shift now is not whether institutions are entering, but how gradually allocations expand over time. If balance sheets of this size continue increasing exposure at a measured pace, the structural bid beneath the market becomes increasingly meaningful.

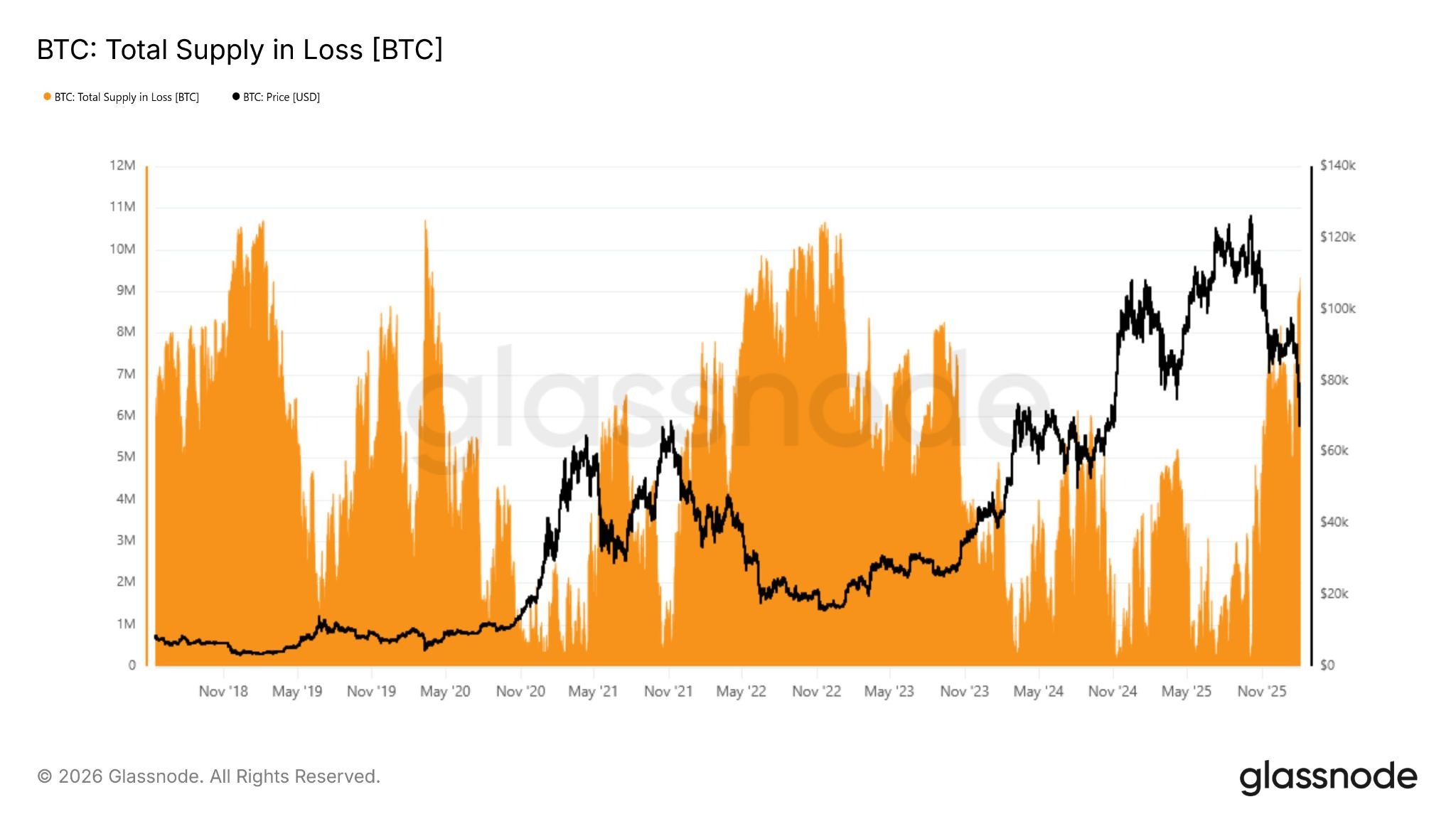

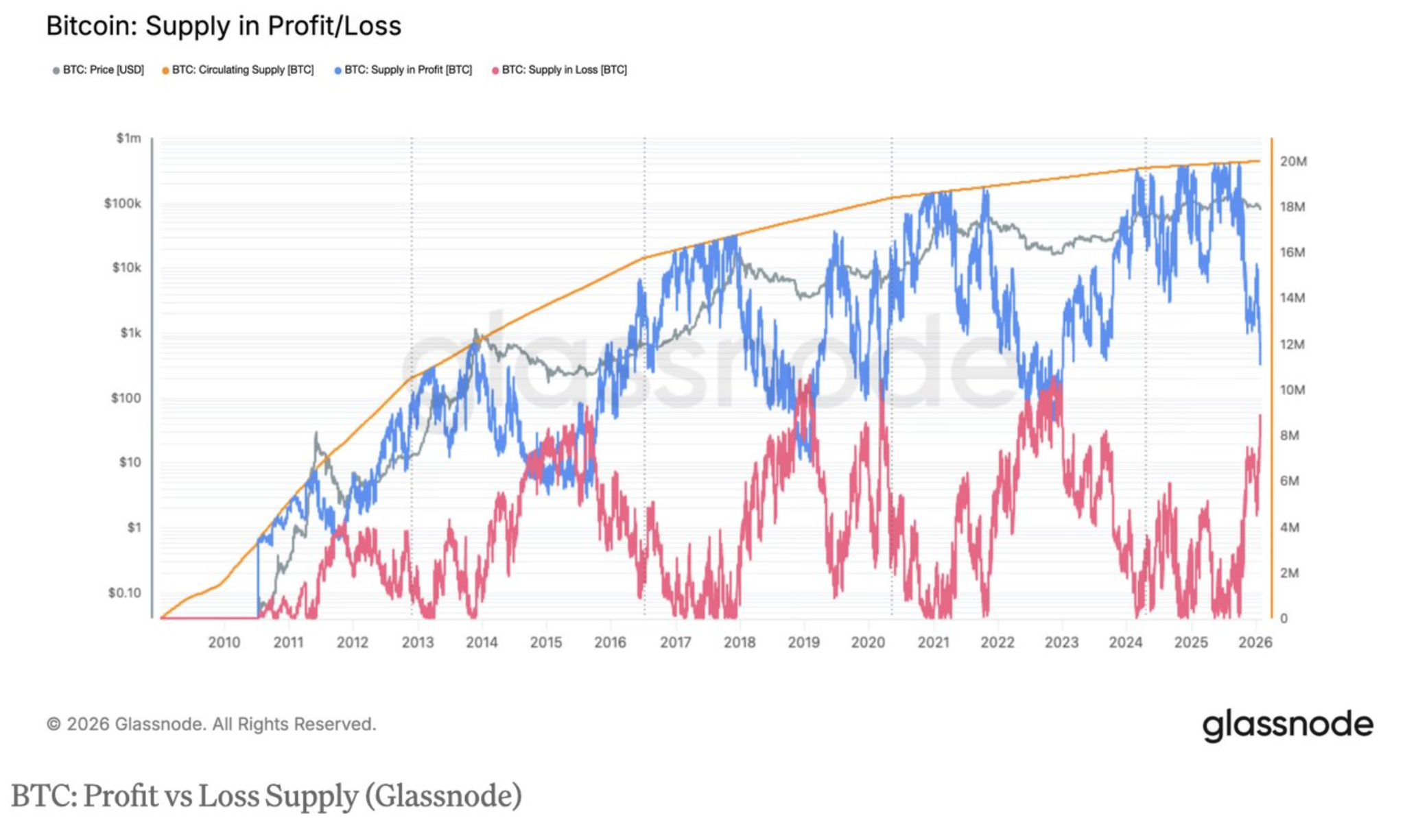

Bitcoin: Capitulation Signals Emerging

Market bottoms tend to show up first in holder behaviour. One of the more useful on-chain metrics right now is Bitcoin supply in profit vs. loss, which measures how much of the ~20M circulating BTC is currently held above or below its last moved price. Spikes in supply held at a loss typically reflect capitulation, weak hands exiting, and selling pressure exhausting.

Historically, major cycle lows have aligned with these peaks. In 2018–2019, more than 10M BTC were held at a loss near the sub-$4K bottom. In 2022, roughly 9–10M BTC were underwater around the $16K low. As of early February 2026, with BTC trading near $64K, approximately 45% of supply (~9M BTC) is now held at a loss.

Another key signal is the compression between supply in profit and supply in loss. Durable bottoms have historically formed when these two measures approach equilibrium, signalling that the majority of weak hands have already been flushed. We’re not fully there yet, but we’re close. That suggests downside risk may be increasingly limited, even if not fully resolved. A deeper sweep toward the $55K region remains possible, but structurally, we are far closer to a bottoming phase than a euphoric top.

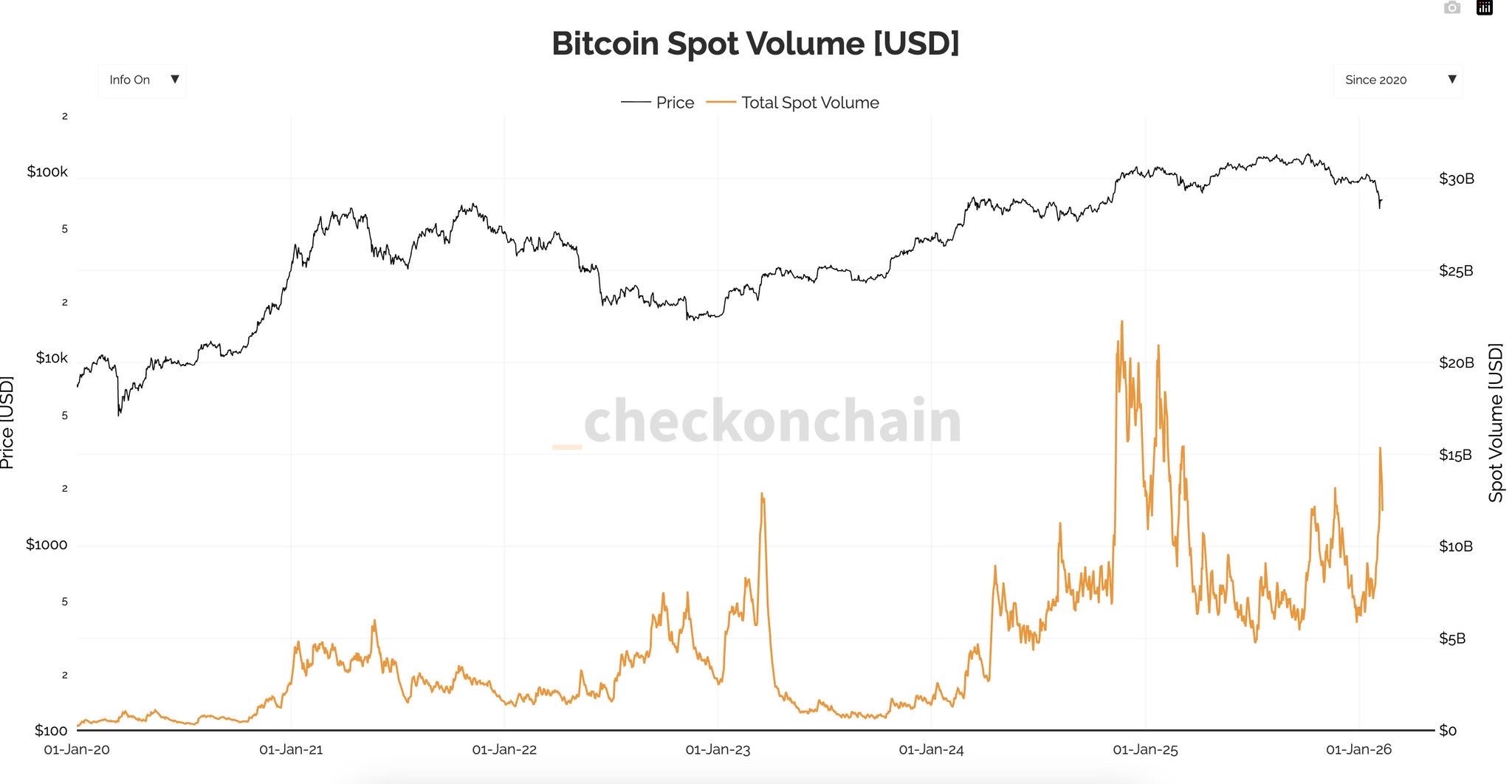

Spot behaviour reinforces this view. During the recent sell-off, spot buying volume expanded aggressively around the ~$60K region, marking the second-largest cluster of spot volume on record, behind only the spike seen during the Trump-driven pump. High spot volume during declines typically signals real capital stepping in, not leverage noise. It reflects demand absorption rather than panic distribution.

Technically, Bitcoin remains in a downtrend. Lower highs continue to form, with resistance sitting beneath the prior cycle ATH around $69K. On the 4H structure, we are watching for a break of this lower-high pattern, until then, rallies can still resolve as continuation moves into lower highs. However, combining technical compression with on-chain capitulation metrics and heavy spot absorption, the asymmetry is shifting. At roughly 45% off the highs, with these signals aligning, the marginal value of further downside is diminishing relative to the potential for stabilisation. This doesn’t confirm the bottom is in. But structurally and behaviourally, this looks far more like capitulation than the beginning of a fresh distribution phase.

Exchange Error Credits Users $40B in BTC

On February 6, 2026, a South Korean cryptocurrency exchange Bithumb made a fatal mistake that contributed to the drawdown of Bitcoin to 60k. During a "random box" promotional event that was supposed to distribute small cash rewards of around 2,000 Korean won (roughly $1.37–$1.50 USD) to eligible users, a human error occurred when an employee mistakenly input the prize amounts in Bitcoin (BTC) instead of Korean won. This caused the system to credit approximately 695 customers with a total of 620,000 BTC, worth over $40-44 billion USD.

Users quickly noticed the huge balances, and some began selling or withdrawing, which triggered a sharp selloff on Bithumb’s BTC/KRW pair. Bitcoin’s price on the exchange briefly crashed by about 15–17% to around 81 million KRW (roughly $55,000 USD). Bithumb detected the error within minutes, restricted trading and withdrawals for affected accounts in about 35 minutes, and started reversing the credits. The exchange ultimately recovered about 99.7% of the mistaken amounts through reversals and user cooperation, leaving around $9 million unrecovered where users had already sold or withdrawn, leading Bithumb to urge voluntary returns and threaten legal action, while confirming that no real on-chain Bitcoin was lost.

Regulators such as the Financial Supervisory Service opened an investigation, and parliament held hearings and demanded stronger internal controls and safeguards at crypto exchanges. Bithumb apologised and stressed it was a human input error rather than a hack and that customer assets were secure. The episode underscored the risks of centralised exchanges, heavy reliance on internal ledgers, and vulnerability to "fat-finger" errors.

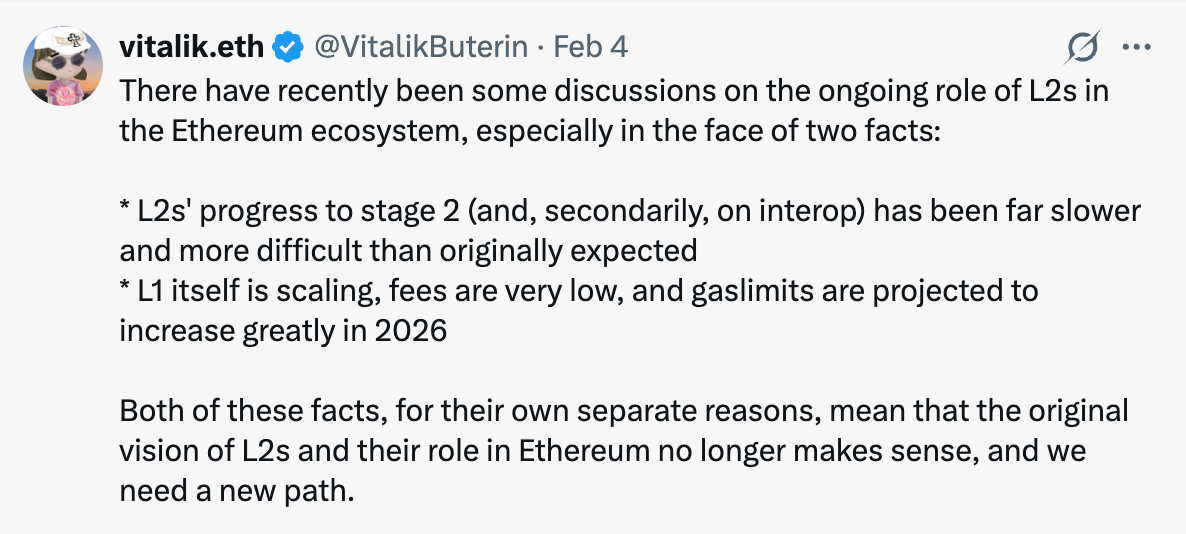

Rethinking the Role of Ethereum Layer 2s

In Vitalik Buterin’s recent X post (ETH Founder), Buterin said that “the original vision of L2s and their role in Ethereum no longer makes sense, and we need a new path,” pointing to slow progress on L2 decentralisation and the fact that Ethereum mainnet is already scaling. At the same time, he has set criteria for which L2s he’ll endorse, focusing on those that evolve beyond being just cheap scaling layers for Ethereum.

Instead, he argues that in order for a Layer 2 to succeed, it needs to offer something L1 cannot easily copy and scale to such as:

- Non‑EVM specialized features or VMs focused on privacy

- Efficiency tailored to a particular application

- Extremely high levels of scaling beyond what an expanded L1 will do

- Totally different designs for non‑financial applications (social, identity, AI)

- Ultra‑low‑latency and other specialized sequencing properties

- Built‑in oracles, decentralized dispute resolution, or other non‑computationally‑verifiable features

This reset suggests the market may become increasingly selective. Generic, copy-paste EVM L2s and governance heavy tokens without clear differentiation could face ongoing pressure if capital continues consolidating into networks that demonstrate stronger technical maturity, clearer user guarantees, and distinct functionality.

The price action of Layer-2 tokens over the past couple years has also reflected its loss of mindshare and product market fit. With most Ethereum L2 tokens quietly slow bleeding

and became some of the worst performers in the market. In 2025, baskets of major L2 tokens like ARB, OP, POL, ZK and STRK fell roughly 75–85%.

General information only. This article is for educational purposes and does not constitute financial, investment, legal or tax advice, nor a recommendation to buy, sell or hold any asset. Cryptocurrency is a high-risk asset and you should consider your own circumstances and seek independent advice before making any decision. Uptrade does not make price predictions.